Introduction

Medical expenses continue to rise, making it crucial for taxpayers to understand which healthcare costs can reduce their tax burden. The IRS allows certain medical expenses to be deducted from your taxable income, but navigating the complex rules and thresholds can be challenging. This comprehensive guide will help you understand qualified medical expenses, the 7.5% AGI threshold, and strategies to maximize your deductions.

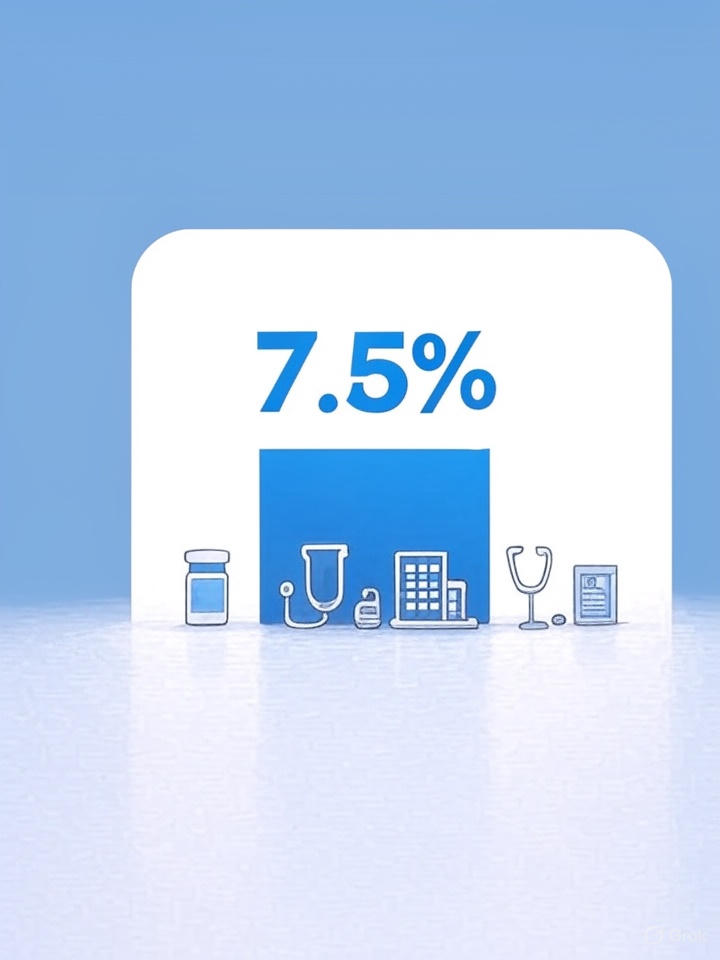

Understanding the 7.5% AGI Threshold

The foundation of medical expense deductions lies in understanding the Adjusted Gross Income (AGI) threshold. Currently, you can only deduct medical expenses that exceed 7.5% of your AGI. This means if your AGI is $50,000, you can only deduct medical expenses exceeding $3,750.

How the Threshold Works

The 7.5% threshold was established to prevent taxpayers from deducting routine healthcare costs while still providing relief for those with significant medical expenses. According to the IRS Publication 502, this threshold applies to most taxpayers filing individual returns.

The calculation is straightforward:

- Calculate your AGI from your tax return

- Multiply by 7.5% (0.075)

- Subtract this amount from your total qualified medical expenses

- The remainder is your deductible medical expense

Qualified Medical Expenses: What Counts

Preventive Healthcare Deductions

Preventive care expenses are fully deductible when they exceed the AGI threshold. These include:

Annual Physical Examinations: Regular check-ups with your primary care physician, including blood work and routine screenings, qualify as deductible medical expenses.

Vaccinations and Immunizations: All vaccines recommended by healthcare professionals, including flu shots, travel vaccines, and childhood immunizations, are considered qualified medical expenses.

Dental Cleanings and Preventive Care: Routine dental cleanings, X-rays, and fluoride treatments fall under preventive healthcare deductions.

Vision Care: Eye exams, prescription glasses, contact lenses, and corrective surgery like LASIK are all deductible medical costs.

Treatment and Therapeutic Services

Tax Deduction for Therapy and Counseling: Mental health services are fully recognized as deductible medical expenses. This includes:

- Psychotherapy sessions

- Marriage counseling

- Addiction treatment programs

- Psychiatric care and medication management

According to Forbes, mental health awareness has increased deduction claims in this category by 25% over the past three years.

Prescription Medications: All prescription drugs prescribed by licensed healthcare providers are deductible, including insulin, heart medications, and specialty drugs.

Medical Equipment and Supplies: Wheelchairs, crutches, blood glucose monitors, and other medical devices prescribed by healthcare professionals qualify.

Alternative Treatments Deductions

The IRS recognizes certain alternative treatments as qualified medical expenses:

Acupuncture: When performed by licensed practitioners for medical conditions, acupuncture treatments are deductible.

Chiropractic Care: Spinal adjustments and related treatments for medical conditions qualify as deductible expenses.

Naturopathic Medicine: Treatments by licensed naturopathic doctors for specific medical conditions are considered qualified medical expenses.

Mileage for Medical Appointments

Transportation costs for medical care are often overlooked but can add up to significant deductions. The IRS allows two methods for calculating mileage for medical appointments:

Standard Mileage Rate

For 2025, the medical mileage rate is 22 cents per mile. This covers:

- Trips to doctors’ offices

- Hospital visits

- Pharmacy runs for prescriptions

- Medical equipment pickup

- Therapy appointments

Actual Expenses

Alternatively, you can deduct actual transportation costs, including:

- Gas and oil directly related to medical trips

- Parking fees at medical facilities

- Tolls paid during medical transportation

Important Note: You cannot deduct general car maintenance, insurance, or depreciation using the actual expense method for medical mileage.

Medical Expense Deduction for Self-Employed Individuals

Self-employed individuals have unique advantages when it comes to medical expense deductions. Unlike traditional employees, self-employed taxpayers can deduct health insurance premiums directly from their income, even if they don’t itemize deductions.

Health Insurance Premium Deduction

Self-employed individuals can deduct 100% of their health insurance premiums for themselves, their spouse, and dependents. This deduction appears on Form 1040 as an adjustment to income, not as an itemized deduction.

HSA Contributions

Health Savings Account contributions are fully deductible for self-employed individuals, providing a triple tax advantage:

- Deductible contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

Home Office Medical Deductions

Self-employed individuals working from home may be able to deduct a portion of home modifications made for medical reasons, such as:

- Wheelchair ramps

- Accessible bathroom modifications

- Specialized lighting for medical conditions

Home Modification for Medical Deduction

Capital improvements to your home for medical reasons can be partially or fully deductible. The key is that the modification must be primarily for medical care.

Fully Deductible Modifications

These improvements have no lasting value to the property and are fully deductible:

- Entrance/exit ramps for wheelchairs

- Grab bars in bathrooms

- Widening doorways for wheelchair access

- Lowering kitchen cabinets for accessibility

Partially Deductible Modifications

Improvements that increase home value are deductible only to the extent they exceed the increased property value:

- Swimming pools for physical therapy

- Elevators for medical mobility

- Central air conditioning for respiratory conditions

The Cleveland Clinic recommends documenting all medical necessity with physician statements for these deductions.

IRS Schedule A Medical Expense Worksheet

Organizing Your Documentation

Proper documentation is crucial for medical expense deductions. The IRS Schedule A medical expense worksheet requires detailed records:

Receipt Requirements:

- Date of service

- Provider name and address

- Type of service provided

- Amount paid

- Insurance reimbursement information

Electronic Records: Digital receipts are acceptable, but ensure they’re stored securely and include all required information.

Common Schedule A Mistakes

Timing Issues: Only deduct expenses paid during the tax year, not when the service was provided.

Insurance Reimbursements: Subtract any insurance reimbursements from the total medical expenses before calculating the deduction.

Cosmetic Procedures: Generally not deductible unless medically necessary for treating disease or improving functioning.

Medical Expense Bunching Strategies

Medical expense bunching involves timing your medical expenses to maximize deductions. Since you must exceed the 7.5% AGI threshold, bunching can be particularly effective.

Timing Strategies

December Payments: Pay for January procedures in December to bunch expenses into one tax year.

Scheduled Procedures: Plan elective but medically necessary procedures in the same tax year.

Prescription Refills: Fill 90-day prescriptions in December rather than waiting until January.

FSA and HSA Coordination

Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) can work alongside medical expense deductions:

FSA Strategy: Use FSA funds for routine expenses and pay for larger procedures out-of-pocket to maximize deductions.

HSA Advantage: HSA contributions are deductible, and qualified withdrawals are tax-free, providing better tax treatment than itemized deductions.

Out-of-Pocket Costs and Insurance Coordination

Understanding how out-of-pocket costs interact with insurance coverage is essential for maximizing deductions.

Deductible Out-of-Pocket Expenses

Deductibles: Health insurance deductibles paid during the tax year are fully deductible.

Copayments: All copayments for medical services qualify as deductible expenses.

Coinsurance: Your portion of covered medical expenses after meeting the deductible is deductible.

Non-Deductible Expenses

Insurance Premiums: Generally not deductible unless you’re self-employed or meet specific criteria.

Cosmetic Surgery: Procedures for appearance improvement rather than medical necessity are not deductible.

Over-the-Counter Medications: Most OTC drugs are not deductible without a prescription.

IRS Publication 502 Guidance: Advanced Strategies

Special Situations

Nursing Home Care: If medical care is the primary reason for nursing home residence, the entire cost may be deductible.

Special Schools: Tuition for schools specifically designed for children with learning disabilities or other medical conditions may qualify.

Service Animals: The cost of buying, training, and maintaining guide dogs or other service animals is deductible.

International Medical Care

Medical expenses incurred outside the United States are deductible if they would qualify as deductible expenses in the US. This includes:

- Emergency medical care while traveling

- Planned medical procedures in other countries

- Prescription medications obtained abroad

Technology and Medical Deductions

Modern healthcare increasingly relies on technology, creating new deduction opportunities:

Medical Apps and Software

Prescription Apps: Apps prescribed by healthcare providers for medical conditions may qualify.

Monitoring Software: Diabetes management apps and similar medical monitoring tools prescribed by physicians are deductible.

Telemedicine Costs

Virtual consultations with healthcare providers are treated the same as in-person visits for deduction purposes.

Planning for Healthcare Professionals

Healthcare professionals have unique opportunities to maximize medical expense deductions while serving their communities. Understanding these strategies can help professionals optimize their tax situation while maintaining high-quality patient care.

For healthcare professionals looking to enhance their practice efficiency, resources like the Health Visitor Toolkit for Professionals provide comprehensive guidance on effective practice management and professional development.

Record Keeping and Audit Protection

Essential Documentation

Medical Records: Keep detailed medical records showing the necessity of treatments and expenses.

Payment Records: Maintain all receipts, canceled checks, and credit card statements for medical expenses.

Insurance Documentation: Keep all Explanation of Benefits (EOB) statements showing what insurance covered.

Audit Preparation

The IRS scrutinizes medical expense deductions more closely than many other deductions. Proper preparation includes:

Physician Statements: Obtain written statements from healthcare providers confirming medical necessity for questioned expenses.

Detailed Logs: Maintain logs of medical mileage, including dates, destinations, and purposes.

Separate Accounts: Consider using a separate bank account or credit card for medical expenses to simplify record keeping.

State Tax Considerations

While federal medical expense deductions follow IRS guidelines, state treatments vary significantly:

State Variations

No State Income Tax: States like Florida, Texas, and Washington don’t tax income, so only federal deductions apply.

Conforming States: Many states conform to federal medical expense deduction rules.

Non-Conforming States: Some states have different AGI thresholds or allowed expenses.

Planning Strategies

Multi-State Considerations: If you have income in multiple states, understand how each treats medical expenses.

State-Specific Benefits: Some states offer additional medical expense benefits not available federally.

Common Mistakes to Avoid

Documentation Errors

Inadequate Records: Failing to maintain proper documentation is the most common mistake leading to denied deductions.

Timing Issues: Deducting expenses in the wrong tax year can trigger audits and penalties.

Calculation Mistakes

AGI Errors: Incorrectly calculating the 7.5% AGI threshold can result in over-claiming deductions.

Double Deductions: Attempting to deduct expenses already reimbursed by insurance or HSA/FSA accounts.

Qualification Errors

Cosmetic Procedures: Deducting cosmetic procedures without medical necessity documentation.

Ineligible Expenses: Including vitamins, supplements, or other non-qualifying expenses.

Future Considerations and Planning

Legislative Changes

Medical expense deduction rules periodically change. The 7.5% AGI threshold was temporarily reduced from 10% and has been made permanent for most taxpayers.

Technology Integration

Emerging healthcare technologies may create new deduction opportunities:

- AI-powered diagnostic tools

- Wearable medical devices

- Virtual reality therapy programs

Planning Strategies

Annual Reviews: Review medical expense deduction strategies annually to ensure optimal tax planning.

Professional Consultation: Consider consulting with tax professionals for complex medical expense situations.

Integration with Retirement Planning: Coordinate medical expense planning with retirement account strategies for optimal tax outcomes.

Conclusion

Medical expense tax deductions provide valuable opportunities to reduce your tax burden while investing in your health. Understanding qualified medical expenses, the 7.5% AGI threshold, and proper documentation requirements is essential for maximizing these deductions.

The key to successful medical expense deductions lies in proper planning, meticulous record keeping, and understanding the complex interaction between insurance coverage, HSA/FSA accounts, and tax deductions. Whether you’re dealing with routine preventive care or significant medical procedures, these strategies can help you optimize your tax situation while maintaining your health and well-being.

Remember that tax laws change frequently, and individual situations vary significantly. Consider consulting with qualified tax professionals to ensure you’re maximizing your medical expense deductions while remaining compliant with current IRS regulations. With proper planning and documentation, medical expense deductions can provide meaningful tax relief during challenging health situations.

For healthcare professionals seeking to enhance their practice effectiveness while managing their own medical expenses, comprehensive resources and professional development tools can provide valuable guidance in both clinical and financial aspects of healthcare management.